Glenn Williams Jr., an equity analyst by background, taps into his knowledge of valuation techniques and price-to-earnings ratios to determine if bitcoin is under or overvalued.

Jennifer Murphy, CEO of Runa Digital Assets explains why digital assets are so important in a broad historical context. She mentions 1771 and how it influenced the development of the market.

– Nick Baker

You are currently reading Crypto Short & LongOur weekly newsletter, containing insights, news, and analysis for professional investors. Register here Get it delivered to your inbox every Sunday

Let’s talk about Bitcoin’s price-to-earnings ratio

Writing this column has been one of my favorite things. I love being able to interact with readers and take them on a journey to learn more about the emerging asset class of crypto. Yes, I do know some things but there’s still so much to learn. I am particularly interested in tying crypto with my traditional finance background (TradFi).

My former job was as an equity research analyst. My main focus was valuation. It was always my goal to get valuation “right”. I tried to answer two related questions.

-

What is an entity worth?

-

Are you able to trade it above or below this amount?

If a company is trading below its projected market value, I would rate it a buy. If it was trading higher, well, it’s probably a sell.

I used a combination fundamental and technical analysis to explore both absolute and relative value techniques. Absolute valuations were determined by the cash flow generated by the company, while relative valuations were calculated based on its relative value to other similar entities or itself at the time.

Bitcoin (BTC), and other crypto assets, don’t produce cash flows that can be used to fund a fundamental analysis. This is unlike companies. Bitcoin is not a company. Bitcoin is a peer to-peer cash system that allows value transfer from one entity into another without the need of third-party validation. This is what people see as valuable, so it’s worth exploring valuations.

Because bitcoin has a fixed supply, many view it as a hedge against devaluation or the actions of inept central bankers. It is both a viable asset class and a place where I can store capital.

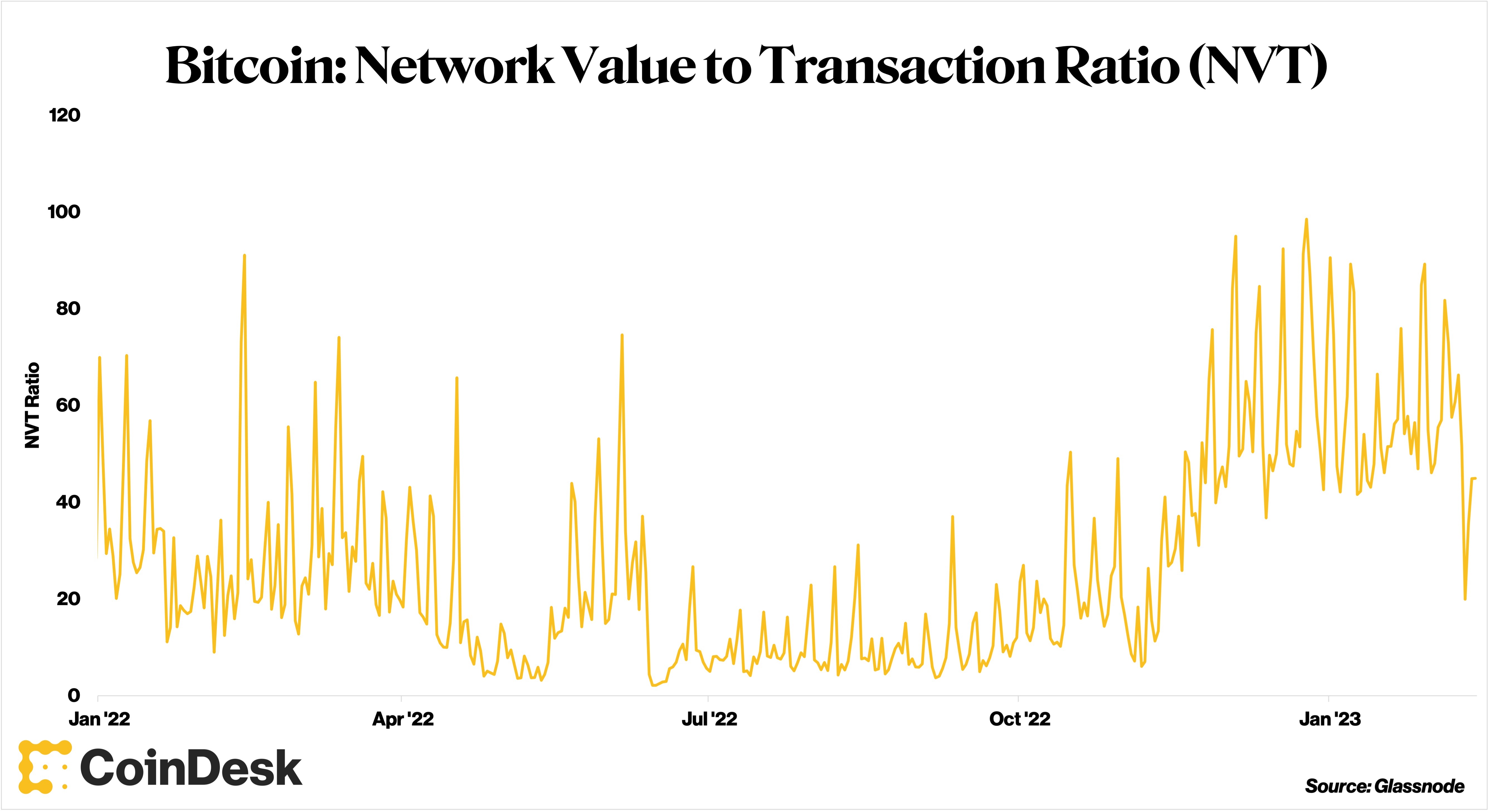

In equities, the most common relative valuation method is price-to-earnings ratios (P/E). Although there are other valuation methods, it gives you a quick comparison of what a company is receiving compared to how much it is earning. The Network Value to Transaction (NVT), which is a crypto version of PE, is the ratio. Willy Woo, a cryptocurrency analyst, developed the metric to measure the relationship between market capitalizations and network transfer volumes. The transfer volume, which is similar to earnings, is simply the count of how many bitcoins are moved from one address into another.

My view is that P/E and NVT must be comparable. Shareholders value earnings, and so does the company. It’s the ability of storing value in a digital asset. This is what I consider space on the blockchain. As demand grows for this space, bitcoin’s value increases. The NVT ratio can be a useful tool in analytic tools if you understand it.

Investors are likely to value bitcoin at a premium if they have high NVT ratios. A low NVT ratio could indicate the opposite. This can make a crypto asset attractive to value investors who prefer to purchase things at discounted prices.

What does it mean to be high or low? What was the date these readings occurred? It’s possible that something which was high-valued one time may be low in the next. This is due to the age of cryptocurrency. It is also sensible to compare where they are to the past. It is also logical to condense the information over specific time periods. It is possible for something that is too valuable in one period to be overvalued in another.

On Aug. 29, 2010, the highest NVT ratio I could find for bitcoin was 448.15. Is it too expensive? BTC traded at 6 cents back then, and now is about $22,000, so I think the relevancy of this reading is somewhat questionable. What if all data prior to 2014 is discarded? This gives us a maximum NVT ratio (98.52), which I believe is more reasonable. Bitcoin’s lowest recorded NVT was 0.22 on January 24, 2016, when BTC traded at $403. This is also relevant because the average NVT for all time periods was 24.

BTC’s NVT at the moment is 44.89. This represents an 82% premium over its average from 2014. It’s 20% lower than its moving averages of 30-, 60-, and 90 days. It is understandable that the average premium for a newer technology such as the Bitcoin blockchain and other new assets would rise over time. It makes sense that the extremes at the high and low ends would shrink, as we have seen with data.

The position you take on the current NVT level is ultimately dependent on where you anchor. BTC may seem overpriced to those who look at its trading history. However, a closer look shows that BTC could be trading at an attractive valuation.

Digital Assets: What Revolutionary Ages and Fat Tails Mean?

The majority of stock market returns are driven by a few winners. The same trend is expected for digital assets.

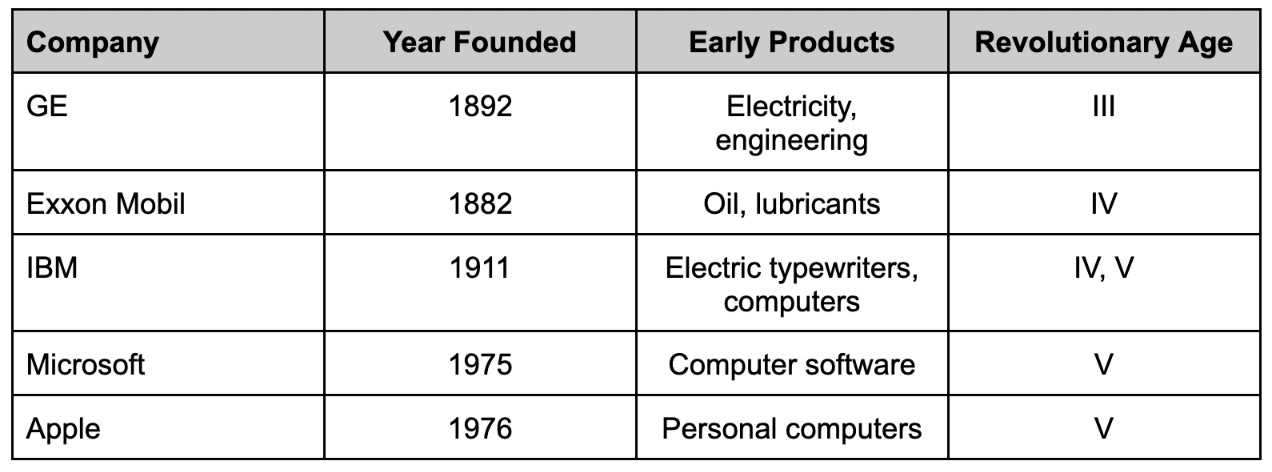

Only five of the 25,300 publicly traded companies that drove 10% of the total wealth creation in the U.S. stock exchange’s $35 trillion between 1926 and 2016 were Exxon Mobil, General Electric (GE), International Business Machines(IBM), Microsoft® (MSFT), and Apple (AAPL). Ninety stocks were responsible for more than half. The entire gain was generated by just shy of 1,100 stocks; the rest returned less than U.S. Treasury Bills.

Why is it so odd?

Stock returns do not fall according to a normal distribution. They tend to skew positive, with some exceptional stocks creating a “fat right tail”. Those stocks were a risk for long-term investors, as they could miss out on the average return of the market.

We expect a large right tail in digital asset return returns. Bitcoin (BTC), is an excellent example of wealth creation. Its returns were compared to market-cap-weighted portfolios of top 10, 50, and 100 digital tokens (excluding stabilizecoins or wrapped tokens), which have been rebalanced every month for the past five years. BTC outperformed all the portfolios. Over the course of the period, both the 50- and 100 token portfolios lost money.

Why? But why?

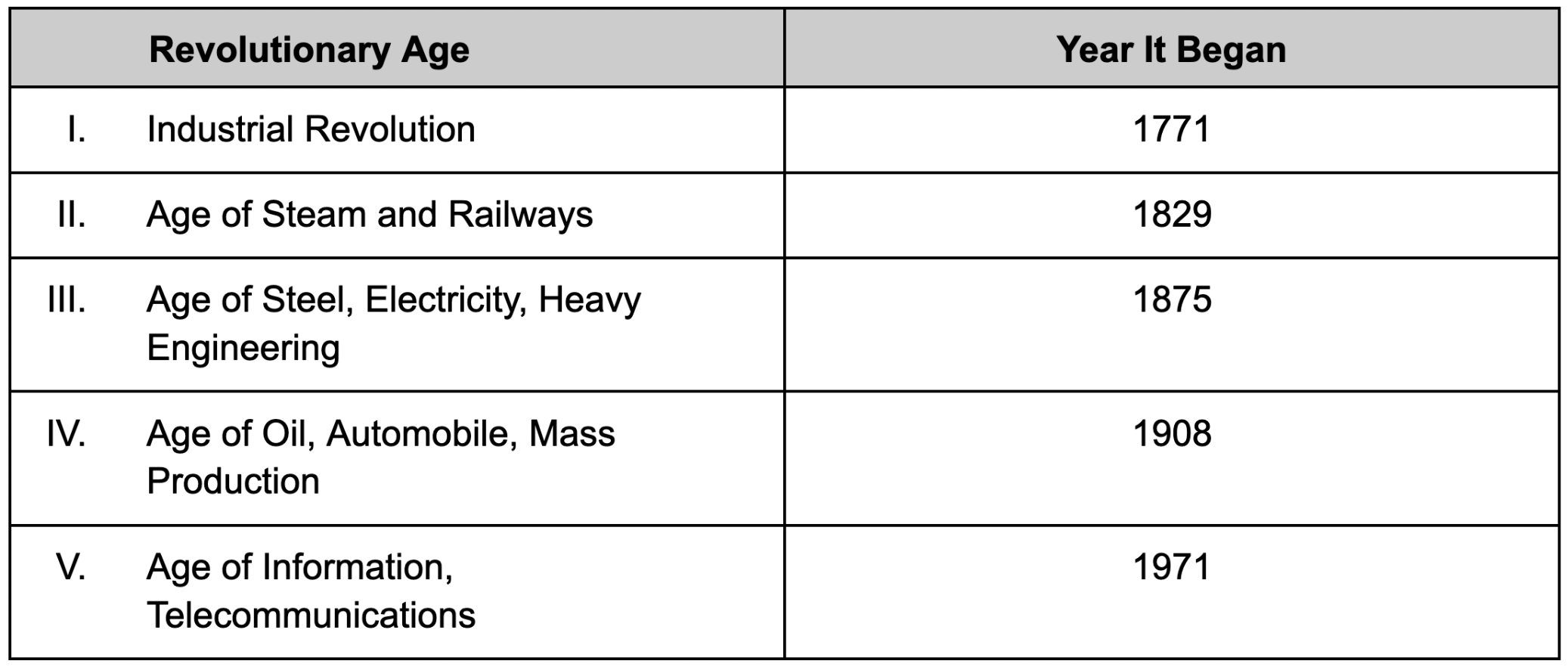

Technological revolutions are a key driver, according to us. Her book is “Technological Revolutions, Financial CapitalCarlota Perez describes these as “a powerful cluster of new and highly visible technologies, products, and industries capable to bring about an upheaval within the entire economy.”

Perez identifies five technological breakthroughs that have occurred since the end of 18th century.

Each period starts with disruptive technological innovations, which attract talent and capital. This creates an explosion of startups. Financial bubbles, corruption, and collapse are common, and eventually bring regulation, management discipline, and productivity, a golden period for growth and profits. Large corporations have dominated the golden periods since the Age of Steel. The greater the chance for winners to accumulate wealth, the longer the golden period.

Five firms that created 10% of all wealth since 1926 were market leaders in a Revolutionary Age.

Each was established at the start of an Age, maximising the potential for compound returns over many years. It wasn’t enough to be there. These winners imagined a better future than others.

The dawning of the Information Age is now more than 50 years ago. A new age is likely to be emerging. It could be the Age of Digital Assets. We believe that digital assets are not sufficient to spark a revolution. However, they are a powerful innovation that can be combined with other innovations such as artificial intelligence robotics and genomics to create a new age.

If we are right, then the newcomers to this Age could be the winners. Long-term investors should ensure that their portfolios contain the wealth creators who will drive the market returns in the future. Digital assets are strong candidates, we believe.

– Jennifer Murphy, CFACEO, Runa Digital Assets

Takeaways

Here’s some news from CoinDesk’s Nick Baker:

-

BIG WEEK This felt like a huge week in the Crypto Regulation and Enforcement Era. Kraken has agreed to close its U.S. Staking Service (news that CoinDesk first broke) in order to settle Securities and Exchange Commission (SEC), charges that the operation offered unregistered securities customers. Brian Armstrong, Coinbase CEO, expressed his concern about any staking crackdown and Gary Gensler, SEC Chair sent a clear warning to Coinbase (and other) that the Kraken case was being investigated. Paxos was then under regulatory scrutiny and said that it would cease issuing Binance’s stablecoin BUSD. It is hard to believe that this is the end of any efforts to curb crypto after the FTX catastrophe.

-

GOOD NEWS! The ethos of decentralization being better than any other is at the heart of crypto. Bitcoin was actually created right after 2008’s financial crisis. The Federal Reserve and other central bank poured money into the financial sector to save it. This upset some of the early backers of crypto. Because individual stakes are not affected by regulatory efforts, the SEC may be trying to remove centralized exchanges from the staking game.

-

BANKING CONUNDRUM The traditional banking system is a long-standing problem for crypto. It’s not been easy. It seems that it is getting more difficult, which adds to the stake issue that has been preventing mainstream adoption of the industry.

-

RUSSIAN SANCTIONS CoinDesk did a great deep dive investigation and found that Russians use crypto to raise money for their troops in Ukraine. This is in spite of sanctions. Add it to the long list of crypto-related activities that are being carried out by global regulators.